Data Center Pricing Continues to Rise as Supply Chain Issues Slow New Development.

After a steady decline in the price of data center space over the last seven years, the average monthly ask rate spiked in 2022, according to the North America Data Center Trends report from CBRE.

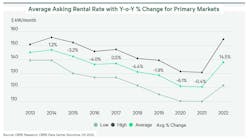

The year-to-year increase in asking price on a kW/month basis by the end of 2022 amounted to 14.5 percent for the wholesale cost of space in the 250-500kW range, to $137.90 per kW/month. And the prices aren’t likely to come down anytime soon, according to the CBRE report for the second half of the year. There are two major factors that will work together to keep prices up; supply chain and power.

From the perspective of supply chain, the impact is surprisingly broad. Everything from materials to construct the physical shell of a data center to the wiring and internal structures has gone up in price and many of the materials have limited availability. This means that schedules are now more at the mercy of individual suppliers than they have ever been before. When materials simply aren’t available, there are few options for contractors looking for ways to hit their deadlines.

This means that projected availability of space in data centers is no longer accurate and customers begin competing for what is available, driving up contract prices. Despite all the issues with new construction, CBRE reports that “the construction pipeline within primary markets increased 153% year-over-year, to 1,839.9 MW.”

These issues also means that as current contracts come to an end, renegotiating those contracts will be impacted by the increased value of the space, especially as operators look to maximize value of existing facilities.

Power Costs and the Bottom Line

The cost of power is now impacting data centers in two ways. The first is the most obvious; the price of energy has gone up, and generally far faster than was expected when existing contracts were signed. In Digital Realty Trust’s recent earnings call, CFO Matt Mercier highlighted the impact of these costs.

“I would say the majority of our contracts are full pass-through," said Mercier. "And even those contracts that are not full pass-through, for the majority of those, we have the ability to pass on price increases, which we either have done or will do soon.” The increase in energy cost should have minimal impact on their bottom line due to the pass throughs.

But with increased focus on renewable energy, power costs will continue to increase and as such, will continue to boost the cost of data center space.

But the actual increase in power generation costs is only part of the power equation. Availability is also a major factor. According to the Turner & Townsend Data Center Cost Index 2022 “78 percent of survey respondents note that delays in securing power supplies has severely impacted delivery dates. To secure a resilient future, the onus is on data center owners and operators to find more efficient, reliable and sustainable means to power these energy-hungry facilities.”

The supply chain problems have impacted the construction of new substations, as well as the deployment of new renewable sources. New data center construction has changed its focus from “where is a geographically desirable location” to “where can I actually get power delivered” in many cases.

The Shifting Geography of Power

Popular data center locations such as Northern Virginia and Silicon Valley are seeing delays in availability that could stretch for years. And they are already space constrained, as the CBRE report notes.

”The overall vacancy rate in primary markets is a record-low 3.2%," the report states. "All primary markets except Silicon Valley saw their vacancy rates fall from a year ago.”

This shouldn’t be read as “out of space” however, as Digital Realty's CEO Andrew Power pointed out in their earnings call, regarding Northern Virginia, that "A large portion of our expected churn happens to be in Ashburn, which is a blessing given the ability to remarket that space at higher and better uses.”

Areas that have power available, such as Atlanta, and the general TVA service area, are seeing an increase in interest from operators looking to construct new facilities. But these locations come with their own cost increases, ranging from significant additional cost in land and taxes to a lack of any other available infrastructure that would need to be built along with the data center.

To many, these costs are not the biggest concern. “In a sector where speed-to-market drives competitive advantage, schedule delays have been wreaking havoc on many data center developments," according to Turner & Townsend’s survey. "For 46 percent of respondents schedule delays are more of a concern than cost or labor issues.” It becomes obvious that scheduling issues touch on everything.

It's clear that the cost of space is likely to continue to increase, simply due to economic factors. But there will also be changes coming to the industry as AI continues to make its mark. Current and next generation AI initiatives take up significant space and power, and as AI becomes a standard application for data center deployment, the cost of operation will rise accordingly.

The demand for compute infrastructure at scale to support AI initiatives is likely the next big thing for data centers and with its power demands and associated infrastructure needs, will focus the industry on building new resources that can meet the power and cooling requirements, at an appropriate price.

About the Author

David Chernicoff

Voices of the Industry