Blue Owl Builds a Capital Platform for the Hyperscale AI Era

Key Highlights

- Blue Owl has transitioned from passive investments to owning and operating digital infrastructure platforms aligned with hyperscale and AI demands.

- The firm’s $7 billion Fund III and partnerships with sovereign wealth funds like QIA signal a focus on long-term, multi-phase AI data center deployments.

- Strategic collaborations with hyperscalers such as Meta and Microsoft showcase a shift towards flexible ownership models that externalize capital while maintaining operational control.

- The industry is experiencing a massive capital buildout, with projected 2026 spending reaching around $600 billion, emphasizing the scale of AI infrastructure expansion.

- Blue Owl’s diversified approach includes developer partnerships, hyperscaler joint ventures, and global development programs, positioning it across multiple deployment pathways.

In earlier coverage, Data Center Frontier examined Blue Owl Capital’s push into data center infrastructure. In the months since, that effort has evolved into something more consequential. What once looked like an extension of a real estate platform now resembles a capital formation engine aligned with the demands of hyperscale and AI infrastructure.

That evolution is not just about scale. It reflects a change in position. Blue Owl has moved into a role where hyperscalers, developers, sovereign investors, and private-wealth channels can all engage through a single platform. Over the past year, more capital managers have begun moving in a similar direction, building integrated strategies to serve what are increasingly programmatic, multi-phase AI deployments. That positioning builds on earlier partnerships, including a joint venture with Chirisa and PowerHouse, where Blue Owl first paired its capital with experienced data center developers to gain exposure to the sector’s growth.

The transition began to take clearer shape with the integration of IPI Partners, which closed on January 6, 2025. The acquisition brought more than $11 billion in assets under management and installed IPI’s Matt A’Hearn as head of digital infrastructure. More importantly, it marked a shift from passive investment toward ownership of an operating and investment platform built around hyperscale relationships. That foundation now underpins Blue Owl’s broader expansion in the sector.

On May 15, 2025, Blue Owl announced the final close of its Digital Infrastructure Fund III at $7 billion, nearly doubling its original $4 billion target and reaching its hard cap. This was not routine fundraising. It signaled that institutional capital is increasingly aligned with the view that AI and cloud demand are driving a long-duration, capital-intensive build cycle. The firm said the fund would focus on developing, acquiring, and owning data centers and connectivity assets, with an emphasis on large-scale build-to-suit projects for hyperscale customers. As Matt A’Hearn put it, size is critical in partnering with hyperscalers:

Size is critical in partnering with hyperscalers and we are incredibly excited to close one of the largest data center-focused funds in the industry. Developing and investing in data centers globally demands expertise and strong end-client relationships. With rising capital needs, staying relevant means having the financial strength to build and own critical digital infrastructure along with maintaining an experienced global team focused on meeting the needs of our partners.

From Projects to Programs: What Fund III Signals

That fundraise matters because it shows Blue Owl is no longer reacting to the AI boom one project at a time. It is aligning its capital strategy with how hyperscalers now build. Those customers increasingly want partners that can fund multi-building campuses, absorb long development timelines, and remain relevant across successive expansion phases.

In that sense, Blue Owl is not just financing data centers. It is positioning itself to finance programs. That distinction matters in AI infrastructure, where individual phases can run into the billions and where balance-sheet credibility can determine whether a campus scales from two buildings to eight, or from one region to several. Variations of this model are now emerging across the market, as other capital providers move to support multi-phase AI deployments at scale.

One of the clearest examples is the Abilene, Texas campus, where Crusoe, funds managed by Blue Owl, and Primary Digital Infrastructure advanced a second phase of development on what has been described as a 1.2-gigawatt AI data center campus. Under the structure, six additional buildings were planned, bringing the total to eight. The second phase began construction in March 2025, with initial energization expected in mid-2026.

The specifications point to how quickly the market is evolving. The buildings have been described as capable of supporting up to 50,000 NVIDIA GB200 NVL72 systems each on a unified network fabric, alongside direct-to-chip liquid cooling and zero-water-evaporation designs. As with many next-generation AI campuses, those figures reflect both ambition and the scale of infrastructure now being contemplated.

Abilene also illustrates Blue Owl’s role in the emerging build model. Rather than operating facilities directly, the firm is providing long-duration capital alongside a developer moving at startup speed and a specialized infrastructure partner. The result is a coalition approach (developer, capital manager, and specialist sponsor) working together to compress timelines on large-scale, greenfield AI campuses.

That structure may have seemed complex in traditional data center finance. In AI infrastructure, it is becoming standard. The scale, power requirements, and system integration challenges are now too large for any single participant to manage efficiently on its own.

It also reflects a broader shift in what is being financed. These projects increasingly resemble industrial capacity more than conventional real estate. At Abilene, Crusoe has said the site supports roughly 3,000 workers on a daily basis, with that number expected to rise significantly during expansion. Early phases represented more than 200 megawatts, with subsequent buildout framed around speed of delivery as much as ultimate scale.

For investors like Blue Owl, that changes the underwriting equation. Execution speed, power delivery, and systems integration now sit alongside traditional real estate metrics. Rent still matters, but the gating factors are land, power, cooling, supply chains, and sponsor capability. And those constraints must be addressed well before construction begins.

From Development Partner to Hyperscaler Counterparty

By early 2026, the Abilene story had become more complex—and more instructive. An Associated Press report on March 27, 2026 said Microsoft had stepped in to partner with Crusoe on two additional AI-focused buildings and an on-site power plant, adjacent to the broader OpenAI-Oracle campus, following OpenAI’s reported withdrawal from part of the project.

According to the report, Crusoe had already completed two buildings tied to OpenAI and Oracle and was continuing work on six more scheduled for delivery by the end of 2026. Microsoft’s planned additions would bring the campus to as many as ten buildings and roughly 2.1 gigawatts of capacity, depending on final buildout.

Blue Owl was not identified as the financier of Microsoft’s expansion. But the shift underscores a larger point: by backing Crusoe early and at scale, Blue Owl positioned itself alongside one of the key developers in the U.S. AI campus buildout. Even as tenant alignments change, the underlying platform continues to attract new capital, customers, and adjacent expansion.

That dynamic points to a broader evolution in Blue Owl’s strategy. The firm is no longer just supporting developers building campuses in search of tenants. It is increasingly participating in structures where hyperscalers themselves are shaping ownership and capital strategy.

That shift is clearest in Blue Owl’s partnership with Meta. On October 21, 2025, Meta announced a joint venture with funds managed by Blue Owl to develop and own the Hyperion data center campus in Richland Parish, Louisiana. Under the structure, Blue Owl-managed funds would hold an 80% stake, with Meta retaining 20%, and both parties committing to fund their pro rata share of approximately $27 billion in development costs across buildings and long-lived power, cooling, and connectivity infrastructure.

Blue Owl contributed roughly $7 billion in cash, while Meta contributed land and construction-in-progress assets and received a one-time distribution of approximately $3 billion. The arrangement reflects a different model of hyperscale expansion—one where ownership, capital deployment, and operational control are increasingly separated.

As Blue Owl Co-CEOs Doug Ostrover and Marc Lipschultz put it:

We're proud that our funds are partnering with Meta on the development of the Hyperion data center campus—an ambitious project that reflects the scale and speed required to power the next generation of AI infrastructure. Blue Owl's ability to deliver substantial capital at scale, combined with our deep experience supporting hyperscalers, makes us uniquely positioned to help bring mission-critical digital infrastructure to life.

Capital as a Service: The Hyperscaler Shift

This is not just another project financing. It points to a model in which hyperscalers can externalize a significant portion of the capital required for AI campuses while retaining operational control. Under the Hyperion structure, Meta provides construction and property management, while Blue Owl supplies capital at scale alongside infrastructure expertise.

Reuters described the transaction as Meta’s largest private capital deal to date, with the campus projected to exceed 2 gigawatts of capacity. For Blue Owl, it marks a shift in role: from backing developers serving hyperscalers to working directly with a hyperscaler to structure ownership more efficiently at scale.

Hyperion also helps explain why this model is gaining traction. Hyperscalers are now deploying capital at a pace that makes flexibility a strategic priority. Structures like the Meta–Blue Owl JV allow them to continue expanding infrastructure without fully absorbing the balance-sheet impact of each new campus.

Analyst commentary cited by Reuters suggested the arrangement could help Meta mitigate risk and avoid concentrating too much capital in land, buildings, and long-lived infrastructure, preserving capacity for additional facilities and ongoing AI investment.

That is the service Blue Owl is effectively providing. Not just capital, but balance-sheet flexibility at a time when AI infrastructure demand is stretching even the largest technology companies. With major tech firms projected to spend hundreds of billions annually on AI infrastructure, that capability is becoming central to how the next generation of campuses gets built.

The Capital Baseline Resets

In early 2026, hyperscalers effectively reset the capital baseline for the sector. Alphabet projected $175 billion to $185 billion in annual capex, citing continued constraints across servers, data centers, and networking. Amazon pointed to roughly $200 billion, up from $131 billion the prior year, while noting persistent demand pressure in AWS. Meta raised its own guidance to between $115 billion and $135 billion, driven by AI infrastructure costs and associated operating expenses.

Taken together, the signal is clear: AI infrastructure is no longer an incremental expansion cycle. It is an industrial buildout measured in hundreds of billions of dollars annually. Reuters placed total planned 2026 spending by major technology firms at roughly $600 billion, underscoring the scale of the shift.

Expanding the Capital Stack: Sovereign Scale

Against that backdrop, Blue Owl has been widening the sources of capital feeding its platform. In September 2025, the firm announced a partnership with the Qatar Investment Authority to establish a digital infrastructure vehicle aimed at accelerating compute capacity for hyperscale customers. The platform launched with more than $3 billion in initial assets and was structured for long-term expansion.

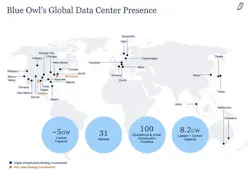

As of mid-2025, Blue Owl said its digital infrastructure strategy had raised $39 billion and invested across more than 100 facilities in nearly 30 markets. The QIA partnership adds a different kind of capital to that base—sovereign wealth with long-duration horizons and tolerance for infrastructure-scale risk.

That matters because AI data centers increasingly require both. These are capital-intensive assets with extended development timelines and uncertain demand curves. By pairing sovereign capital with its existing funds and permanent capital strategies, Blue Owl is building a deeper reserve to support multi-phase hyperscale deployments.

Multiple Paths to the Same Outcome

Blue Owl is not relying on a single model to deploy that capital. With Crusoe, it is aligned with a developer integrating energy and compute at startup speed. With Meta, it is participating directly in hyperscaler-led campus ownership. With STACK Infrastructure, it is paired with an experienced global operator capable of executing across multiple markets.

This diversification creates optionality. Rather than committing to a single build paradigm, Blue Owl is positioning itself across several: hyperscaler joint ventures, developer-led campuses, and globally scaled development programs. Each reflects a different path to the same outcome, delivering capacity at the scale and speed AI demand now requires.

There is also a consistent pattern in where the firm chooses to operate. Blue Owl is concentrating on the most constrained parts of the market: hyperscale customer concentration, capital intensity, power procurement, and deployment timelines. Those are higher-risk positions than stabilized wholesale assets. But they are also where the strategic value is shifting in the current cycle.

Execution at Scale: The STACK Layer

The firm’s relationship with STACK Infrastructure adds an execution layer to that strategy. In March 2025, STACK secured $6 billion in green financing across campuses in Stafford, Portland, and Toronto, bringing total debt capital raised for its global portfolio to roughly $20 billion. Later that year, STACK and Blue Owl advanced plans for a next-generation AI campus in Doña Ana County, New Mexico, described as exceeding 1 gigawatt and incorporating on-site power and closed-loop cooling.

Together, these efforts point to a coordinated approach: capital at scale, multiple deployment pathways, and operating partners capable of executing large, complex builds. That combination is increasingly what it takes to remain relevant in the AI infrastructure cycle.

Where the Model Gets Tested

In early April, that broader capital backdrop showed signs of strain. Bloomberg reported that Blue Owl limited redemptions from two of its private credit funds after facing unusually large withdrawal requests, including roughly 22% of shares in one vehicle and more than 40% in another.

The move follows similar actions by peers across the private credit sector, as investors grow more cautious amid concerns about credit quality and exposure to technology and software companies, some of which are now being reshaped by the same AI wave driving data center demand.

That selectivity is also showing up at the project level. Late in 2025, reports indicated that Blue Owl declined to back Oracle’s planned $10 billion data center campus in Michigan, amid lender concerns about debt levels and evolving market conditions. While details remain limited, the decision suggests that even the largest AI infrastructure projects are not immune to stricter underwriting as capital providers reassess risk.

This is not a digital infrastructure event in itself. But it is a reminder that the capital supporting AI buildouts does not exist in isolation. It flows through broader markets that can tighten quickly, particularly in segments tied to private wealth and income-oriented investors.

For a firm like Blue Owl, now operating across institutional funds, sovereign partnerships, hyperscaler joint ventures, and private wealth channels, that linkage matters. Access to capital is not just about scale. It is about stability, duration, and investor confidence across multiple funding sources.

Against that backdrop, Blue Owl’s trajectory over the past year is clear. The firm has moved from participant to platform: integrating IPI, scaling its flagship fund, expanding its role in Abilene alongside Crusoe, forming a sovereign-backed partnership with QIA, opening additional channels through private-wealth vehicles such as ODIT, and entering a direct hyperscaler joint venture with Meta at Hyperion.

The model is built to match the scale of AI infrastructure demand. The question now is whether the model can hold under the same market pressures shaping the capital behind it. In the AI buildout, access to capital matters, but the ability to deploy it at speed may be what ultimately separates the leaders from the rest.

At Data Center Frontier, we talk the industry talk and walk the industry walk. In that spirit, DCF Staff members may occasionally use AI tools to assist with content. Elements of this article were created with help from OpenAI's GPT5.

Keep pace with the fast-moving world of data centers and cloud computing by connecting with Data Center Frontier on LinkedIn, following us on X/Twitter and Facebook, as well as on BlueSky, and signing up for our weekly newsletters using the form below.

About the Author

David Chernicoff

Voices of the Industry